How I Transferred Money to Spain to Buy a Property and Paid Zero in Fees

When you’re buying property in Spain as a UK buyer, one of the least glamorous but most consequential decisions you’ll make is how to move your money. The purchase price, the ITP tax, the notary fees — all of it needs to arrive in euros, in Spain, on time. And the method you choose will either cost you hundreds of pounds or nothing at all.

We converted the full purchase sum for our Alicante property in summer 2025. We paid zero in conversion fees. Here’s exactly how, and how it compares to the main alternatives.

What Most People Do (And What It Costs)

The default for most UK buyers is a high street bank transfer. It feels safe and familiar. It is also, by a significant margin, the most expensive option.

A typical UK bank charges 2 to 3% on international currency transfers, plus a fixed transfer fee of £15 to £30. On a £50,000 conversion that’s £1,000 to £1,500 in fees before you’ve even started. On a £200,000 purchase it’s potentially £4,000 to £6,000 gone before you’ve paid a single Spanish tax.

Nobody tells you this clearly. It’s buried in exchange rate margins rather than listed as a fee. Your bank gives you a rate that looks like the real rate but is quietly 2 to 3% worse than the mid-market rate you’d see on Google. That gap is their profit, and on a property purchase it adds up to a painful amount.

The Two Alternatives Worth Considering

Wise

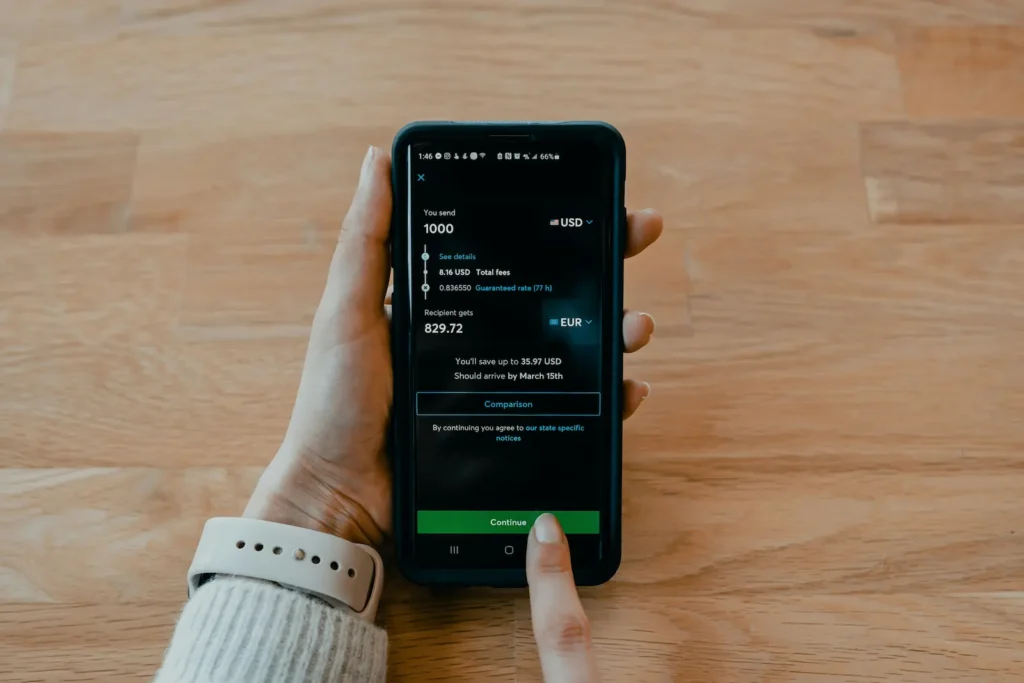

Wise (formerly TransferWise) is the most straightforward option for a one-off large transfer. It uses the mid-market exchange rate and charges a transparent percentage fee that you can see before you commit.

I ran a live comparison in March 2026: sending £25,000 via Wise would deliver €28,883, with a total fee of £77.84, which works out at 0.31%. The rate was guaranteed for 24 hours. Arrival time: seconds.

That’s honest, transparent, and considerably cheaper than any bank. For most UK buyers making a single large transfer to complete a Spanish property purchase, Wise is probably the best option available.

Revolut Business

Revolut Business charges 0.6% on foreign exchange above a €1,000 monthly free allowance. On the same £25,000 transfer, it delivered €28,801 after a fee of around £145 equivalent, meaningfully more expensive than Wise for a large one-off conversion.

However, there’s a version of Revolut that changes this calculation entirely.

What We Actually Did: Revolut Metal

At the time of our purchase we were both on Revolut’s Metal plan, their premium personal tier, currently £14.99 per month, which includes fee-free currency exchange with no monthly cap.

We converted in two tranches rather than all at once. The first portion was converted on a day when the rate was favourable, then held in euros ready for completion. The remainder stayed in GBP earning interest in the meantime, and was converted closer to completion day. Both conversions were fee-free on Metal.

The euros were then transferred into a Revolut Business account and distributed to the sellers on completion day, six separate payments, all EUR to EUR, all local transfers, all free.

Total conversion fees on the full purchase sum: £0.

When to Convert: Timing Your Transfer

This is something most guides skip, but timing can make a bigger difference than fees. The GBP/EUR rate moves daily, and on a large sum even a small shift matters. A 1% move on a £100,000 transfer is £1,000, which is more than Wise’s entire fee.

There are a few decision points where timing comes into play.

Before or after signing the arras contract? The arras deposit (typically 10% of the purchase price) is your first large payment. You’ll need euros in your account to pay it. If you wait until the arras is signed before even thinking about currency, you’re rushing and may convert at a bad rate. I’d recommend having at least the deposit amount already converted to euros before you sign anything.

All at once or in stages? Converting everything in one go is simpler, but you’re locking in a single rate. Splitting the conversion into two or three tranches, as we did, spreads the risk. If the rate moves against you on one tranche, you might catch it moving back on the next. This isn’t a guaranteed strategy and you could equally end up worse off, but it reduces the chance of converting your entire purchase price on the worst day of the month.

Rate alerts. Both Wise and Revolut let you set rate alerts. Pick a target rate and you’ll get a notification when it hits. This takes the emotion out of the decision and means you’re not checking the rate every morning over breakfast.

The key thing is to start thinking about currency well before you need the money. Once you’ve found a property and are heading towards an arras, the clock is ticking.

Source of Funds: The Compliance Step Nobody Mentions

Here’s something that catches UK buyers off guard. Both Wise and Revolut are legally required to verify the source of large transfers. This is standard anti-money-laundering compliance, not a problem, but if you don’t know it’s coming it can cause delays at exactly the wrong moment.

For property purchases, you’ll typically need to provide bank statements showing where the money came from, plus documentation of the transaction itself. Wise has a specific process for large transfers where they may ask for your property contract, proof of savings, or salary evidence. Revolut can flag large movements for review too.

What this means in practice: don’t leave your first large transfer to the day before completion. Do a test transfer of a smaller amount (say £1,000) a few weeks ahead to trigger any verification requirements early. Get your documents uploaded and approved while you still have time. Then when you need to send the full amount, the path is already clear.

I wish someone had told me this before we started. We didn’t have any issues, but I’ve heard from other buyers who had transfers held for review at the worst possible time because they hadn’t done the compliance step in advance.

The Honest Comparison

Here’s what each option would cost on a £25,000 conversion (based on live rates I checked in March 2026):

High street bank: £500 to £750 in hidden rate margin plus a fixed fee of £15 to £30.

Revolut Business: approximately £145, charged as 0.6% above the €1,000 monthly free allowance.

Wise: £77.84, charged as a transparent 0.31% fee at the mid-market rate.

Revolut Metal (personal): £0, fee-free up to fair use limits.

The differences scale proportionally. On a £100,000 purchase, the bank option could cost you £2,000 to £3,000. Wise would be around £310. Revolut Metal would still be £0.

The Catch With Revolut Metal

Revolut Metal costs £14.99 per month. If you’re upgrading purely for a property purchase conversion, factor that in. On any meaningful transfer the saving still vastly outweighs the subscription cost, even a single month’s subscription pays for itself many times over on a property-sized transfer.

One important note: Revolut applies a fair usage limit on fee-free exchange. For very large transfers it’s worth checking current Metal plan limits before relying on this approach. The limit resets monthly, so large conversions can be spread across months if your timeline allows. We converted in two tranches partly for this reason.

Beyond the Purchase: Ongoing Transfers

The purchase price transfer gets all the attention, but it’s not the last time you’ll need to move money to Spain. Once you own the property, there’s a steady stream of ongoing costs that need paying in euros: community fees, IBI tax, insurance premiums, gestor invoices, maintenance, and anything else that comes up.

If your property is generating rental income through a Spanish SL, most of these costs are paid from the company’s euro account and you may not need to transfer from the UK at all. But if you’re holding the property personally, or if the rental income doesn’t cover everything, you’ll be making regular smaller transfers.

For ongoing transfers, the equation shifts. Wise is still excellent for ad-hoc payments. Revolut Business with its €1,000 monthly free allowance works well for routine costs that stay under that threshold. And if you’re on Metal personally, the fee-free conversion continues to apply.

The point is that currency transfer isn’t a one-time decision. It’s an ongoing part of owning property in Spain, and getting the right setup in place from the start saves money every month, not just on the day you buy.

What I’d Recommend

If you’re making a large one-off transfer and don’t already use Revolut: use Wise. It’s transparent, fast, and considerably cheaper than any bank. Set up your account early, do the source of funds verification ahead of time, and you’ll be ready to move quickly when you need to.

If you’re already on Revolut Metal or can justify the subscription: convert on personal Metal, send via Business. It’s what we did and it cost nothing.

If you’re buying through an SL company, as I did, think about your banking setup holistically. The currency transfer is one piece, but the day-to-day account and how you manage ongoing costs all connect.

Whatever you do, don’t use your high street bank for currency conversion. The margin they take is quietly significant and entirely avoidable.

This article contains affiliate links for Wise. I only recommend services I have personally used. Using these links costs you nothing extra and helps support this site.