Most people lose hundreds on currency conversion when buying abroad. Here’s what we did instead, and how it compares to the alternatives.

When you’re buying property in Spain as a UK buyer, one of the least glamorous but most consequential decisions you’ll make is how to move your money. The purchase price, the taxes, the notary fees — all of it needs to arrive in euros, in Spain, on time. And the method you choose will either cost you hundreds of pounds or nothing at all.

We converted the full purchase sum for our Alicante property in summer 2025. We paid zero in conversion fees. Here’s exactly how, and how it compares to the main alternatives.

What Most People Do (And What It Costs)

The default for most UK buyers is a high street bank transfer. It feels safe and familiar. It is also, by a significant margin, the most expensive option.

A typical UK bank charges 2–3% on international currency transfers, plus a fixed transfer fee of £15–£30. On a £50,000 conversion that’s £1,000–£1,500 in fees before you’ve even started. On a £200,000 purchase it’s potentially £4,000–£6,000 gone before you’ve paid a single Spanish tax.

Nobody tells you this clearly. It’s buried in exchange rate margins rather than listed as a fee.

The Two Alternatives Worth Considering

Wise

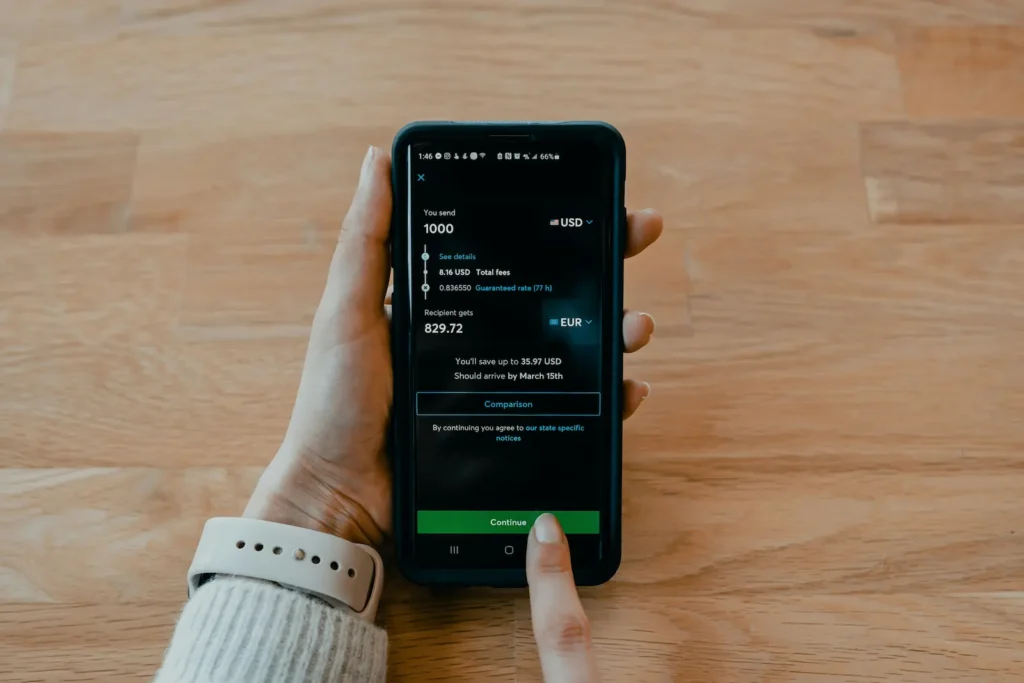

Wise (formerly TransferWise) is the most straightforward option for a one-off large transfer. It uses the mid-market exchange rate and charges a transparent percentage fee.

I ran a live comparison in March 2026: sending £25,000 via Wise would deliver €28,883, with a total fee of £77.84 — 0.31%. The rate was guaranteed for 24 hours. Arrival time: seconds.

That’s honest, transparent, and considerably cheaper than any bank.

Revolut Business

Revolut Business charges 0.6% on foreign exchange above a €1,000 monthly free allowance. On the same £25,000 transfer, it delivered €28,801 after a fee of around £145 equivalent — meaningfully more expensive than Wise for a large one-off conversion.

However, there’s a version of Revolut that changes this calculation entirely.

What We Actually Did: Revolut Metal

At the time of our purchase we were both on Revolut’s Metal plan — their premium personal tier, currently £14.99/month — which includes fee-free currency exchange with no monthly cap.

We converted in two tranches rather than all at once. The first portion was converted on a day when the rate was favourable, then held in euros ready for completion. The remainder stayed in GBP earning interest in the meantime, and was converted closer to completion day. Both conversions were fee-free on Metal.

The euros were then transferred into a Revolut Business account and distributed to the sellers on completion day — six separate payments, all EUR to EUR, all local transfers, all free.

Total conversion fees on the full purchase sum: £0.

The Honest Comparison

| Fee on £25,000 | Fee type | |

|---|---|---|

| High street bank | £500–£750 | Rate margin + fixed fee |

| Revolut Business | ~£145 | 0.6% above €1k allowance |

| Wise | £77.84 | 0.31% flat |

| Revolut Metal (personal) | £0 | Fee-free up to fair use limit |

The Catch (And It’s a Small One)

Revolut Metal costs £14.99/month. If you’re upgrading purely for a property purchase conversion, factor that in. On any meaningful transfer the saving still vastly outweighs the subscription cost.

One important note: Revolut applies a fair usage limit on fee-free exchange. For very large transfers it’s worth checking current Metal plan limits before relying on this approach. The limit resets monthly, so large conversions can be spread if your timeline allows.

What I’d Recommend

If you’re making a large one-off transfer and don’t already use Revolut: use Wise. It’s transparent, fast, and considerably cheaper than any bank.

If you’re already on Revolut Metal or can justify the subscription: convert on personal Metal, send via Business. It’s what we did and it cost nothing.

Whatever you do: don’t use your high street bank for currency conversion. The margin they take is quietly significant and entirely avoidable.

Already thinking about the banking setup for your Spanish property? Why I Ditched Spanish Banks and Use Revolut Business Instead covers how I manage day-to-day finances for the Elche flat — and why I never opened another traditional Spanish account after Sabadell.